Wood Mackenzie’s answers future-facing commodities questions

Wood Mackenzie’s second annual Future Facing Commodities Forum took a deep dive into the outlook for the materials key to building our electrified future. It explored the status and outlook of electric vehicle (EV) penetration, renewables power generation and storage, the outlook and costs of disruptive technologies and the impact on key commodity markets.

During the event, Wood Mackenzie invited attendees to send them their most pressing questions. Perhaps unsurprisingly, risks to demand forecasts featured heavily, highlighting the uncertainty associated with the energy transition.

The most common topics centred around five broad themes:

- Battery technology change

- Substitution

- Scrap evolution

- Decarbonisation policy impacts

- The viability of hydrogen technologies

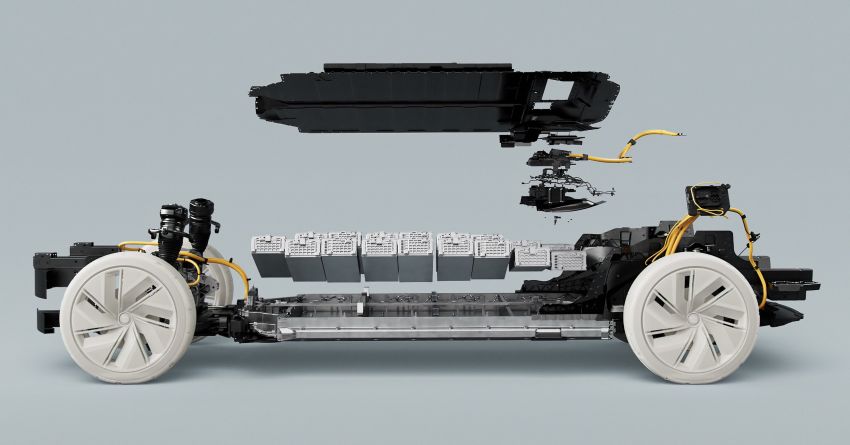

Where is the greatest potential impact for lithium demand?

The development and adoption of existing Li-ion cathode chemistries will have a large impact on lithium demand in the coming decades, since different chemistries require a varying amount of lithium in their compositions.

For instance, lithium iron phosphate (LFP) uses less than half the lithium of nickel manganese cobalt (NMC) batteries. And a cathode chemistry switch is certainly an option for OEMs to relieve demand pressure on lithium.

However, there are limitations to the adoption of using certain technologies. For example, LFP cathodes are typically used in lower-performance EVs. In the longer term, sodium-ion (Na-ion) batteries and fuel cells offer possible alternatives to lithium. We would need to see significant improvement in Na-ion technologies (cell-to-pack and cell-to-chassis engineering) for its viability in the >40 kWh EV market. Meanwhile, Na-ion energy densities are considerably lower than other Li-based batteries.