ArcelorMittal South Africa reports on its operations

The company’s average capacity utilisation increased from 42% in H1 2022 to 53% in 2023. Crude steel production increased by 29%, or 305 000 tonnes, from 1.05 million to 1.36 million tonnes for the first six months of 2023. Crude steel production was unchanged against the immediately preceding six months.

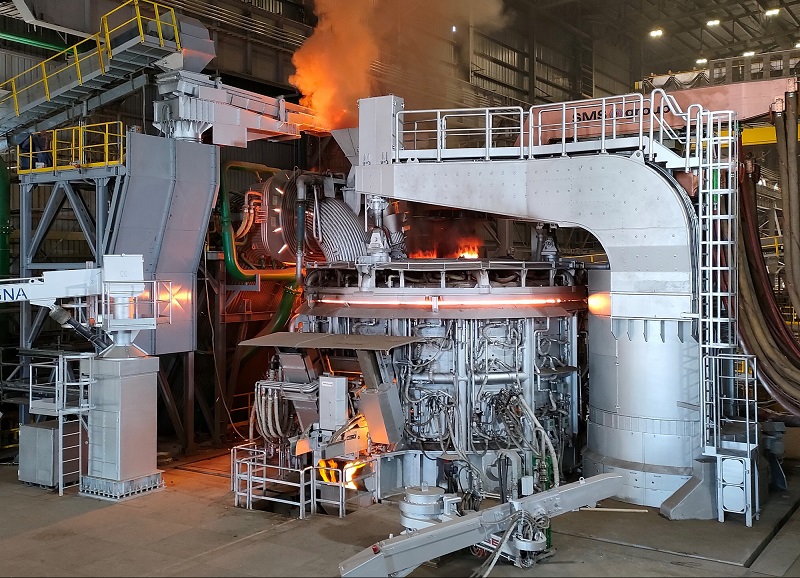

As previously reported, the fourth quarter of 2022 saw the start-up of one of the blast furnaces at Vanderbijlpark being delayed due to weak domestic demand. The hot blast stove restoration programme is currently underway on the second blast furnace. The blast furnace in Newcastle is performing well, however, extreme rain conditions (resulting in flooding) disrupted production on several occasions.

For H1 2023, commercial coke production was 85% lower at 9 000 tonnes, with sales volumes down by 83% at 20 000 tonnes due to the previously communicated continuing restoration of the coke batteries. A meaningful recovery is expected from 2025 onwards.

The company’s raw material basket (iron ore, coking coal and scrap), representing 48% (H1 2022: 43%) of cash cost per tonne, was 2% up in rand terms, compared to a 13% decrease in the international basket. The local basket was flat in rand terms compared to the immediately preceding six months.

Consumables and auxiliaries represent 31% of cash cost per tonne (based on crude steel production) (H1 2022: 31%). Electricity tariffs increased by 14%, while dollar-denominated commodity-indexed consumables decreased by 12%.

Fixed costs increased from R3 448 million in H1 2022 to R3 549 million for the period under review, an increase of 3%. Fixed costs increased by 11% (H2 2022: R3 196 million) in the immediately preceding six months.

Outlook for the second half of 2023

Internationally, the World Steel Association expects a 2.2% increase in steel demand. Chinese GDP growth will continue to play a role in international steel demand and pricing trends. According to the South African Reserve Bank, 2023 GDP is expected at 0.4%.

Steel demand is expected to improve as economic indicators strengthen. Inflation is moving back towards the target range of between 3-6% which should lessen the pressure on interest rates and assist with lifting consumer confidence.

Renewables and regional infrastructure projects are expected to support steel demand. Exchange rates will continue to have an impact as will rail service and electricity reliability.

ArcelorMittal South Africa is positioned to navigate the immediate and near-term challenging market conditions while remaining focused on its medium to longer-term objectives.